Medicare Advantage growth has been one of the most significant shifts in U.S. healthcare over the past decade. For healthcare CFOs, that shift is no longer just a payer-mix footnote. It is now a central driver of your organization’s financial performance.

Today, more than 35 million Americans are enrolled in a Medicare Advantage (MA) plan, representing over half of all Medicare-eligible beneficiaries. And according to the Congressional Budget Office, that share is projected to grow from 54% in 2024 to roughly 64% within the next ten years.

That is a massive patient population flowing through private-plan rules, not traditional fee-for-service Medicare. And with it comes a complex web of financial opportunities and revenue cycle landmines.

This blog breaks down what Medicare Advantage growth means for CFOs in concrete, actionable terms. We cover where the money is, where it is at risk, and how to protect it.

Why Medicare Advantage Growth Matters More Than Ever to Your Bottom Line

Medicare Advantage is no longer a niche segment. It is the mainstream. KFF reports that MA covered 54% of eligible Medicare beneficiaries in 2025, with enrollment rising from just 8 million in 2007 to over 35 million today.

For provider organizations, this means:

- A larger share of your patient volume is tied to MA contracts

- Reimbursement no longer follows uniform federal fee-for-service rules

- Each MA plan has its own billing requirements, prior authorization rules, and reimbursement logic

The financial stakes are high. Hospitals spent $43 billion in 2025 trying to collect payment from insurers for care already delivered, with nearly $18 billion spent on overturning claims denials alone. A significant portion of that burden falls squarely on MA claims.

If your organization is not actively managing its MA revenue cycle strategy, you are almost certainly leaving money on the table.

The Financial Opportunities CFOs Should Be Capitalizing On

Medicare Advantage growth is not all headwinds. There are real, tangible financial opportunities for organizations that position themselves correctly.

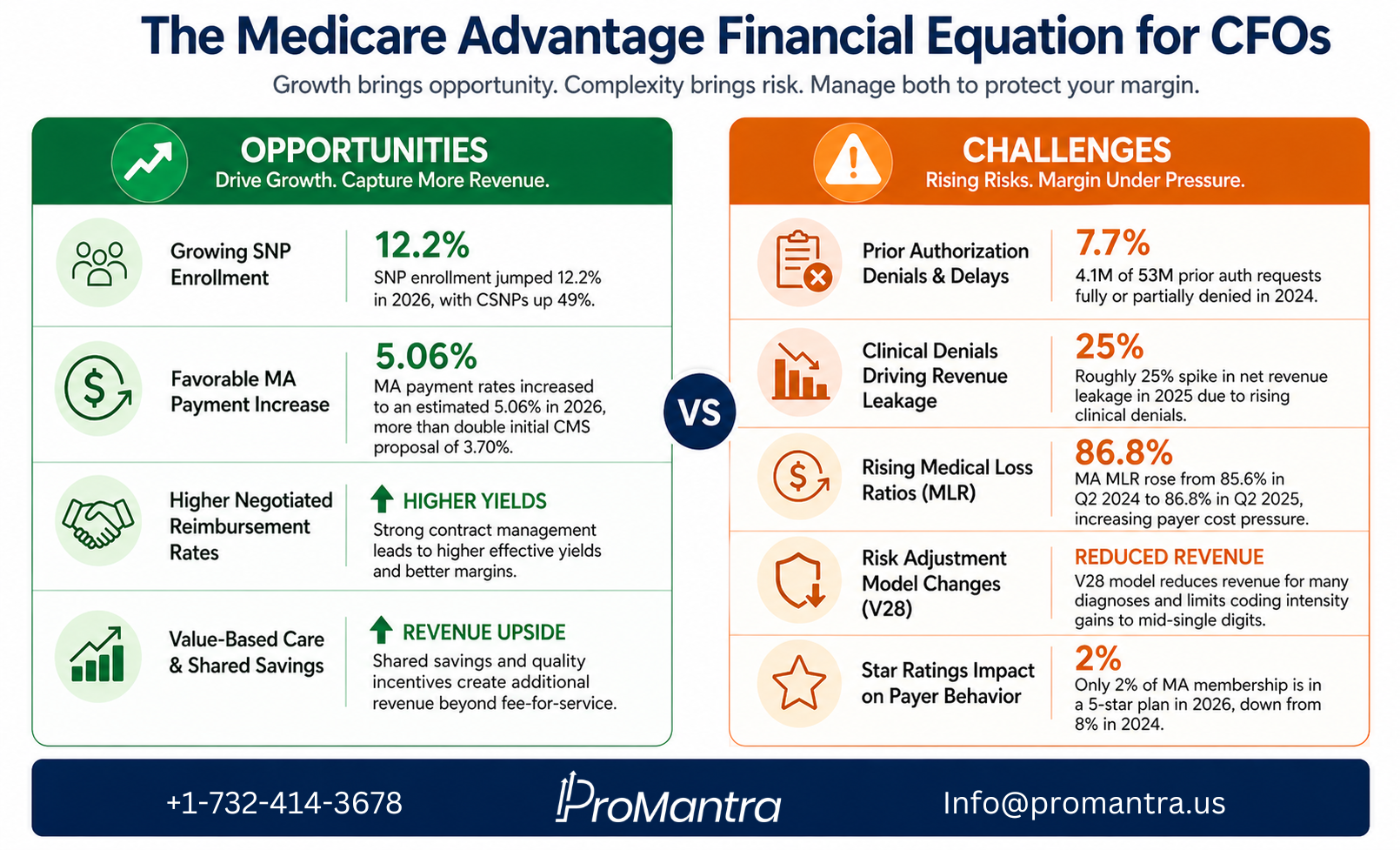

1. Higher Negotiated Reimbursement Rates

Unlike traditional Medicare, MA plans allow room for negotiation. Providers with strong contract management practices consistently achieve higher effective yields.

Provider organizations that realize higher yields from negotiated rates tend to manage performance from a foundation of strong revenue cycle activities, including regular contract reviews and payer scorecards (Forvis Mazars, 2024).

If your contracts have not been renegotiated in the past 12 to 24 months, you may be underperforming against what the market will support.

2. Growing Special Needs Plan (SNP) Enrollment

SNP enrollment jumped 12.2% in 2026, led by an explosive 49% increase in Chronic Condition SNPs (CSNPs). More than one in five MA enrollees now has coverage through an SNP (HealthScape Advisors, 2026).

For providers serving high-acuity populations, SNPs represent a higher-revenue patient cohort. Capturing this volume requires precise clinical documentation to support accurate risk adjustment coding, which translates directly into better reimbursement.

3. Favorable MA Payment Rate Increases

The current administration increased MA payment rates to an estimated 5.06%, more than double what CMS initially proposed at 3.70% (Georgetown Medicare Policy Initiative, 2025). This favorable policy shift gives providers breathing room on the reimbursement side.

Capturing this uplift requires accurate documentation and clean claims submission. Plans only pass higher revenue to providers when documentation justifies the risk scores.

4. Value-Based Care and Shared Savings Potential

Many MA contracts now include shared savings arrangements tied to quality and cost outcomes. For CFOs willing to invest in care coordination and population health management, these arrangements can generate significant upside revenue beyond standard fee-for-service payments.

The Financial Challenges CFOs Cannot Afford to Ignore

The same Medicare Advantage growth that opens revenue doors also creates serious financial risks. Here is where most providers are losing margin.

1. Prior Authorization Denials and Delays

Medicare Advantage insurers made nearly 53 million prior authorization determinations in 2024. Of those, 4.1 million were fully or partially denied, representing 7.7% of all requests (KFF, 2024).

For your revenue cycle team, each denial means rework, delayed cash, or lost revenue. The administrative cost of managing prior auth at this scale is not small.

Organizations without payer-specific prior authorization workflows will continue to absorb this cost without any visibility into how to fix it.

2. Rising Medical Loss Ratios and Payer Margin Pressure

Medical loss ratios in MA rose from 85.6% in Q2 2024 to 86.8% in Q2 2025 (NAIC via Georgetown, 2025). When payers are squeezed, they push that pressure downstream to providers through tighter utilization management, more aggressive audits, and slower claims adjudication.

The result for CFOs? Longer reimbursement cycles, increased denial activity, and more administrative work to collect the same dollar.

3. Risk Adjustment Model Changes (V28)

CMS has phased in its updated risk adjustment model (V28), which reduced revenue for many common diagnoses and tightened guardrails on coding intensity. Even the most sophisticated coding operations can now only reach mid-single-digit gains from risk adjustment (PwC, 2025).

For providers, accurate clinical documentation is more important than ever. Undercoded charts mean underpayment. There is no shortcut around this.

4. Star Ratings Impact on Payer Behavior

Only 2% of MA membership is enrolled in a 5-star plan in 2026, down sharply from 8% in 2024 (HealthScape Advisors, 2026). Plans with lower Star Ratings receive smaller quality bonus payments, which reduces their rebate dollars.

As payers lose bonus revenue, they compensate by tightening provider payments. CFOs need to understand which payers in their network are under Star Rating pressure, because those plans are most likely to increase denial activity.

5. Clinical Denial Activity Is Rising Fast

A review of over 2,300 hospitals found a roughly 25% jump in net revenue leakage in 2025 due to rising clinical denials. Payers are increasingly requiring providers to prove medical necessity, driving higher final denials even when care was clinically appropriate.

This is not just a billing problem. It is a documentation and clinical coding problem that your CFO strategy needs to address at the source.

What High-Performing CFOs Are Doing Differently

The organizations navigating Medicare Advantage growth most successfully share a few common practices.

They maintain payer scorecards. Tracking MA plan performance by denial rate, days to payment, and effective yield gives revenue cycle teams the data they need to escalate contract issues and prioritize appeals.

They invest in documentation integrity. Clinical documentation improvement (CDI) programs tied directly to risk adjustment coding are not just a compliance measure. They are a revenue strategy.

They build payer-specific workflows. Each MA plan has different rules. Organizations with customizable workflows for prior authorization, billing edits, and appeals significantly outperform those relying on generic processes.

They treat contract management as a C-suite priority. Managing MA contracts is a significant time investment, often falling on the CFO or CEO, but the potential increase in revenue from strong contract compliance makes it essential. This is not a task to delegate without executive oversight.

They partner with specialized RCM experts. As Medicare Advantage growth continues to reshape payer mix, the complexity of managing it in-house increases. Strategic outsourcing to an RCM partner with MA expertise has become a margin-preservation strategy, not just a cost play.

How ProMantra Helps Healthcare Organizations Navigate Medicare Advantage Growth

At ProMantra, we specialize in revenue cycle management for healthcare providers navigating exactly this kind of complexity. We understand that Medicare Advantage growth creates unique billing, coding, and payer management challenges that generic RCM solutions are not built to handle.

Our team brings deep expertise in:

- MA-specific denial management and appeals, with payer-level intelligence built into every workflow

- Clinical documentation improvement (CDI) programs that support accurate risk adjustment coding

- Contract performance monitoring and payer scorecard management

- Prior authorization management across multiple MA plans and service lines

- End-to-end revenue cycle support that scales with your growing MA patient volume

We work with health systems, physician groups, and specialty practices across the country to protect and optimize their MA reimbursement. Whether your challenge is rising denials, undercoding, or payer contract performance, ProMantra has the expertise and process infrastructure to close the gap.

Frequently Asked Questions (FAQs)

Q1: Why is Medicare Advantage growth a financial concern for healthcare providers?

Medicare Advantage growth means more of your patients are covered under private plans with their own billing rules, prior authorization requirements, and reimbursement structures. Unlike traditional Medicare, MA plans can deny claims, impose utilization management, and delay payments in ways that directly impact your cash flow and operating margin.

Q2: How does risk adjustment coding affect Medicare Advantage reimbursement for providers?

Risk adjustment coding determines the acuity score of MA patients, which influences how much CMS pays to the MA plan, and in turn how much the plan reimburses the provider. Inaccurate or incomplete clinical documentation leads to lower risk scores and underpayment. With CMS now using the V28 risk model, accurate coding is more critical and more restricted than before.

Q3: What should a CFO prioritize to improve Medicare Advantage revenue cycle performance?

CFOs should prioritize payer-specific workflow development, clinical documentation integrity, prior authorization tracking, denial management with root cause analysis, and regular contract performance reviews. Maintaining a payer scorecard by MA plan is one of the most actionable first steps to identify where revenue is leaking.

Q4: Is outsourcing Medicare Advantage RCM a smart financial decision?

For most provider organizations, yes. The administrative complexity of managing multiple MA plans, each with unique rules and billing requirements, has made in-house management increasingly expensive and error-prone. Partnering with an experienced RCM firm like ProMantra that specializes in MA billing and denials management can reduce administrative costs, lower denial rates, and accelerate cash flow.

The CFO Takeaway

Medicare Advantage growth is not slowing down. Enrollment has already crossed 35 million beneficiaries, representing 51% of the Medicare population, and the CBO projects that figure will reach 64% within the next decade.

The question is not whether MA will dominate your payer mix. It already does for most providers. The question is whether your revenue cycle infrastructure is built to capture what you are owed from it.

Opportunities exist in negotiated rates, SNP volume, favorable policy changes, and value-based arrangements. But those opportunities are only realized by organizations that get the operational details right: prior authorization, documentation, coding, denials management, and contract compliance.

For CFOs who treat their MA revenue cycle as a strategic priority, the growth of this market is a competitive advantage. For those who do not, it is a slow financial leak that compounds quarter over quarter.

Ready to Strengthen Your Medicare Advantage Revenue Cycle?

ProMantra’s RCM experts help healthcare providers capture every dollar they earn from Medicare Advantage plans. From denial prevention to contract optimization, we deliver the operational depth your finance team needs.

Request a Free RCM Consultation with ProMantra Today.